Group Retirement Benefits Redesign

Reimagined self-serve and agent-supported journeys related to group retirement benefits, encompassing onboarding, defining retirement goals and a savings strategy, managing contributions, and preparing to retire.

I led research, strategy, and concept design work for all journeys and helped assemble and coach a newly formed digital product team to begin iterative delivery of these improved journeys. This work formed a critical pillar in the client’s national group plan strategy and was reaffirmed with further investment and support every year from 2020 to the present.

My responsibilities:

Generative research

Service & product strategy

Conceptual design & testing

Agile team coaching & delivery

Project length:

16 weeks

10

Journeys reimagined

87

“Signature moment” high-impact features defined

12

Weeks to deliver MVP of new client onboarding journey

+$150M

Growth in total assets under management connected to impacted journeys

Context

A major Canadian insurance company was losing market share to competitors in their group benefits and retirement investment products as a result of perceived poor-quality digital service capabilities. The poor quality experience was deemed directly responsible for the loss of a $1B account in 2016. As a result, they wanted to reimagine their group retirement benefits services to improve the experiences of plan members and administrators.

Concepts

How I delivered impact

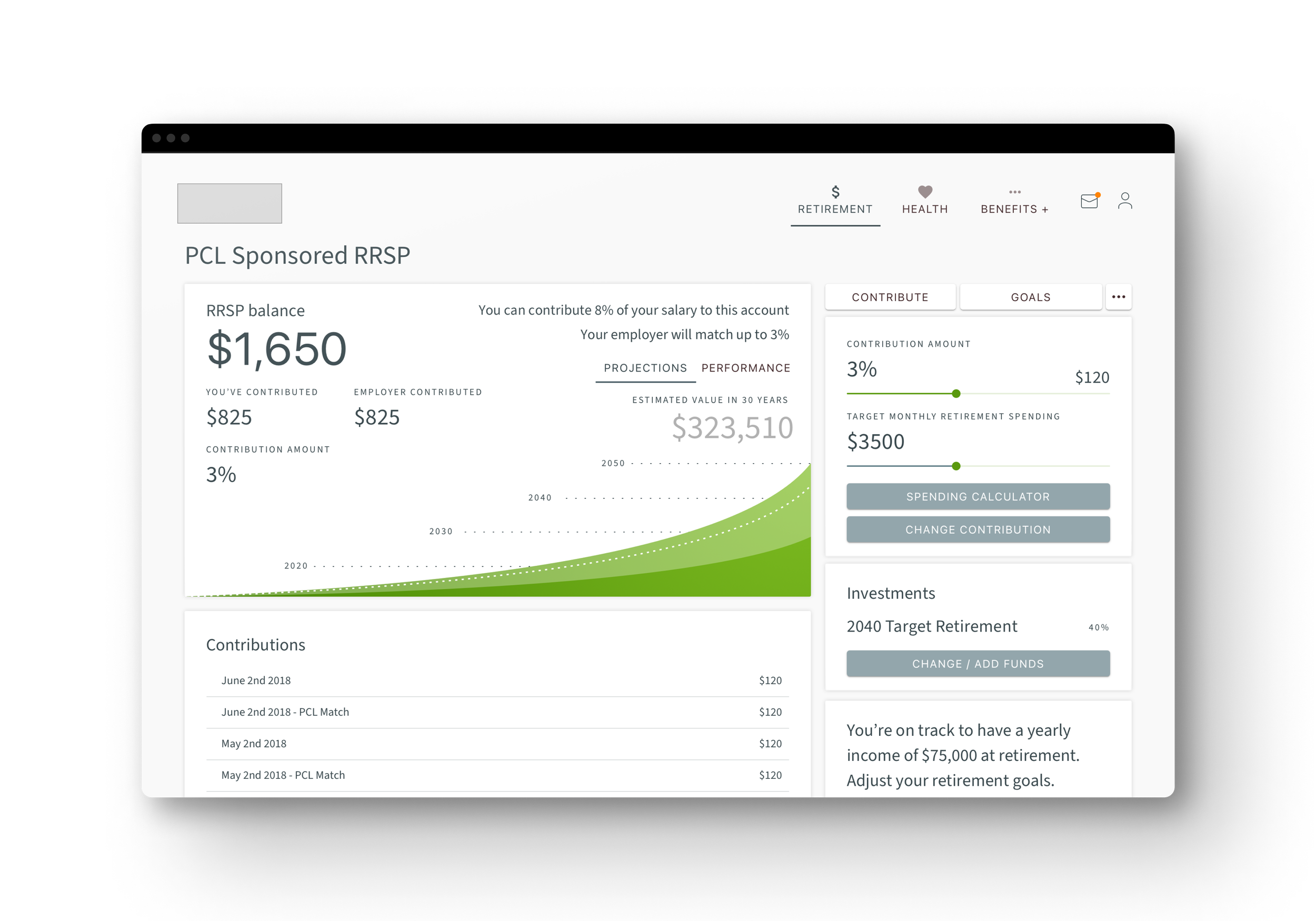

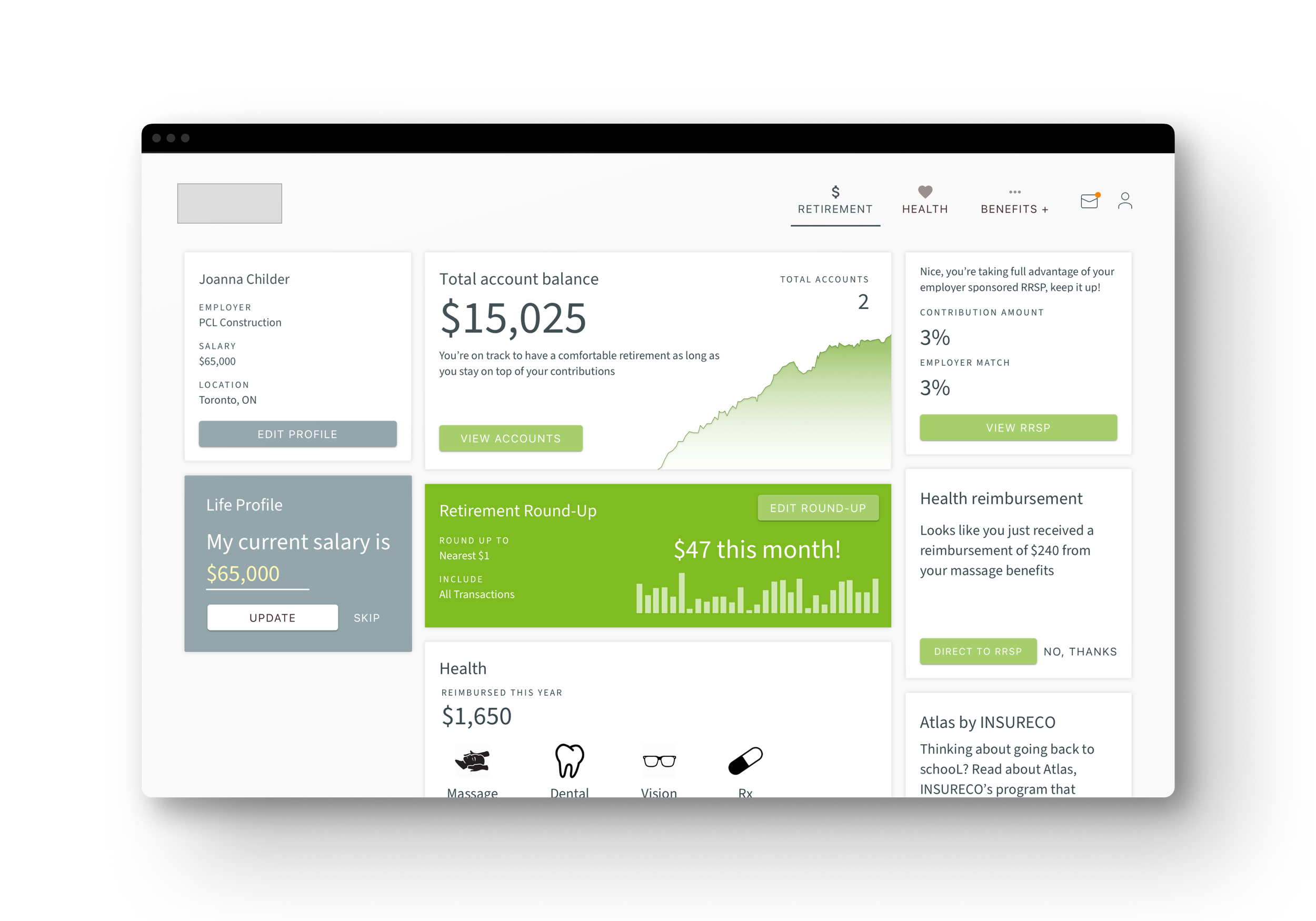

Smart nudges: Leveraging behavioural nudges to achieve business outcomes

I designed many of the features for these products with the mental models and propensities of the client’s plan members (and people in general) when it comes to retirement savings in order to be able to nudge them to take positive actions to improve their retirement preparedness. These actions were also strongly aligned with the clients’ business objectives, in that they generally drove greater participation and higher deposits in their accounts. In our research, we found many plan members were both sheepish about not contributing as much as they felt they should and uncertain about what was “normal” to contribute. By simply highlighting when a plan member’s monthly contribution amount was less than the majority of others, this simultaneously provided a meaningful benchmark and provided a little social pressure to increase to meet that amount.

Hybrid testing: Moving beyond prototypes to gauge actual behaviours

It is easy for participants in testing to act on something like increasing monthly contributions to a retirement fund because they are ultimately not beholden to that decision moving forwards and there is no financial benefit or loss to be felt. To try and gauge actual behaviours and responses, we worked with advisors and leveraged prototypes augmented with real data in real advisory conversations to compare outcomes. We also tried gamification using part of the participant incentive payment to evaluate whether messaging was driving desired behaviours.